Wondering if you need to pay tax on your cryptocurrency in the UK? or how to file to file Bybit Taxes in the UK, Check out our easy-to-follow UK Crypto Tax guide! Learn all about how the UK taxes crypto activities, including DeFi, mining, and staking. Plus, we’ll share some top tips on how to lower your UK crypto tax bill. Whether you’re trading on Bybit or curious about your tax obligations. We’ve got all the info you need on “Bybit tax in the UK” – all simplified for you, with Catax helping you along the way.

- What is the tax rate for cryptocurrency transactions in the UK?

- How to pay taxes on cryptocurrency in the UK?

- Is HMRC Track your Transaction?

- UK’s Crypto Capital Gains

- UK’s Crypto Capital Gains Tax rates

- Steps to Calculate crypto gains and losses

- Calculate CGT on cryptocurrency UK

- Here’s a friendly step-through-step to see if you made a profit or a loss:

- What Happened of tax on lost or stolen crypto in the UK

- Do I have to pay taxes when buying crypto?

- Do I have to pay taxes when buying crypto?

- What About Adding or Removing Liquidity?

- How are airdrops and forks taxed in the UK?

- Navigating Crypto Mining and DeFi Taxes in the UK

- What kind of records might HMRC ask for?

- How Can I avoid my Crypto taxes in the UK?

- Navigating Your Bybit Taxes in the UK with Catax: Simple Steps

- Why This Matters in the UK:

Do I need to pay tax on my cryptocurrency in the UK?

Yes, most crypto investors in the UK will need to pay taxes on their digital assets. In the UK, banks and financial bodies don’t see crypto as cash or currency. Instead, tax-wise, crypto gets the same treatment as stocks and shares, meaning it’s taxable. The HMRC (Her Majesty’s Revenue and Customs) states that depending on your crypto transactions. You might have to pay Capital Gains Tax Income Tax, or sometimes both.

So, if you’re trading on Bybit or any other platform, you’ll likely have to deal with “Bybit tax in the UK”. And remember, Catax can help make figuring out your crypto taxes a lot simpler.

What is the tax rate for cryptocurrency transactions in the UK?

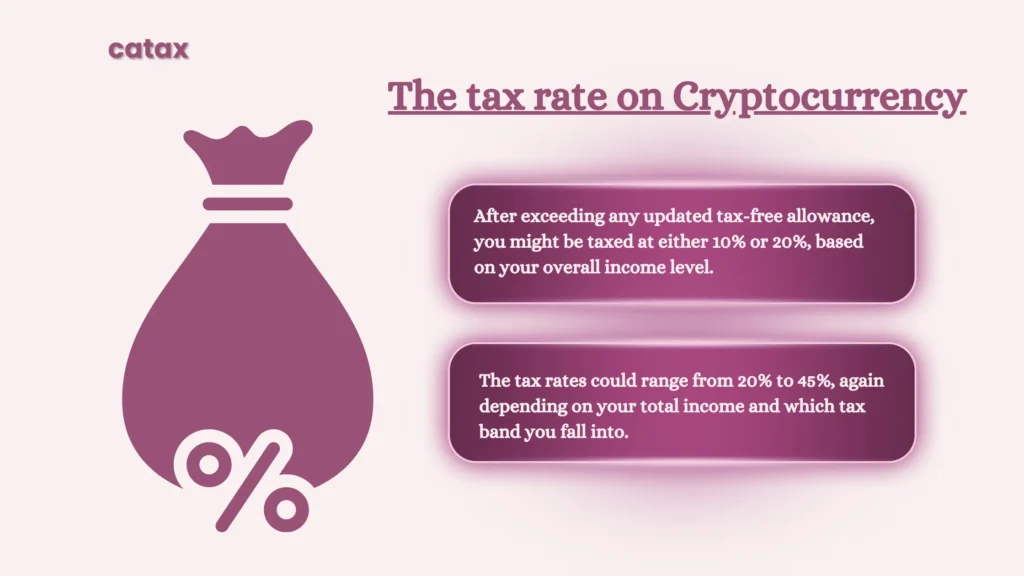

To file Bybit Taxes in the UK, if your profits from crypto go beyond the £12,300 tax-free limit. You’re looking at a tax rate of either 10% or 20% for capital gains. If you earn additional income from crypto that exceeds your allowance. The tax rate ranges from 20% to 45%, depending on the type of transaction, the applicable tax, and which Income Tax bracket you’re in.

For the Financial Year 2024-2025:

To file Bybit Taxes in the UK, Bybit users, and other crypto investors must note that the tax-free allowance for capital gains was £6,000 in the 2023-2024 financial year. HMRC will specify any changes to this allowance for 2024-2025 in their updates.

When it comes to capital gains from crypto:

- After exceeding any updated tax-free allowance, you might be taxed at either 10% or 20%, based on your overall income level.

For additional income from crypto:

- The tax rates could range from 20% to 45%, again depending on your total income and which tax band you fall into.

How to pay taxes on cryptocurrency in the UK?

To file Bybit Taxes in the UK, you must know how to pay taxes on your crypto earnings, crypto investors in the UK can either report their gains on their annual self-assessment tax return or utilize HMRC’s real-time CGT reporting service.

Keeping accurate records is essential for all self-employed individuals, including crypto investors who must maintain precise records for tax purposes.

According to HMRC, crypto investors are required to declare the following:

- The types of tokens they have.

- The dates they disposed of the tokens.

- The Quantity of tokens disposed of.

- The remaining quantity of tokens.

- The value of the tokens in pounds sterling.

- Bank statements and wallet addresses.

- Records of pooled costs before and after disposal.

Ensuring compliance with Bybit Tax in the UK involves adhering to these requirements and maintaining detailed records to accurately report earnings and transactions. By partnering with Catax, investors can receive expert guidance on reporting gains, maintaining accurate records, and leveraging available tax-saving strategies. With Catax’s expertise, investors can confidently navigate the tax landscape and optimize their financial position in the crypto market.

Additional Tips for UK Bybit Users:

- Stay Informed: Cryptocurrency tax laws can evolve. Keep updated on HMRC guidelines related to crypto assets.

- Deductible Expenses: Remember, certain costs associated with acquiring, holding, and selling crypto can be deducted. Catax can help identify these.

- Capital Gains Allowance: For the 2023/2024 tax year, the capital gains tax allowance is £12,300. Any gains beyond this threshold are subject to tax. Note that this allowance is set to change in future years, so always check the latest figures.

- Record-Keeping: Maintain detailed records of all your Bybit transactions for at least five years after the January 31st submission deadline of the relevant tax year.

Remember, crypto gains in the UK count as Capital Gains Tax (CGT), so don’t forget to report them on your annual tax return. But hey, there’s an even smoother option: HMRC’s real-time CGT reporting service lets you pay tax as you go!

Is HMRC Track your Transaction?

You must have this question while filling out your Bybit Taxes in the UK, the answer is yes. Indeed, HMRC can keep an eye on your cryptocurrency activities. They have partnerships with UK exchanges, such as crypto.com, enabling them to closely monitor crypto transactions and identify those who are not up to date with their taxes.

- HMRC collaborates with all UK-based exchanges for data sharing.

- They have access to crypto transaction details going back to 2014.

- HMRC knows the personal details (KYC) you provided when you registered with any UK exchange or wallet.

- Recently, HMRC has encouraged crypto holders to come forward and voluntarily report any unpaid taxes on their crypto assets. They’ve introduced a new service for this purpose. If you don’t reach out to HMRC, you might face extra charges and penalties.

This move indicates HMRC’s increasing attention to crypto taxes and their efforts to uncover undeclared earnings, especially as the UK prepares to share information with European countries about crypto transactions under CARF regulations.

Regarding how far back HMRC might look to find undeclared gains, it depends on how accurately you’ve reported your taxes:

- If you’ve been careful with your crypto tax reports but missed some payments, you’ll need to disclose and settle taxes for the last four years.

- If you haven’t been careful enough in reporting your crypto profits, you’re expected to pay back taxes for up to six years.

- If you’ve intentionally avoided paying the correct amount of tax on your crypto gains or income, you might need to declare and pay any due taxes for up to 20 years.

So, it’s clear that staying on top of your “Bybit Tax in the UK” and being transparent with HMRC about your crypto dealings is crucial to avoid any future headaches.

UK’s Crypto Capital Gains

HMRC treats cryptocurrency as a capital asset, which means when you part ways with your crypto in any form, it’s time to think about Capital Gains Tax (CGT). This includes various scenarios like:

- Selling your crypto for British pounds or any other traditional currency.

- Swapping one cryptocurrency for another, including stablecoins.

- Using crypto to purchase items or services.

- Giving away crypto as a gift, except to your spouse or civil partner.

When you engage in these activities, you’re liable for CGT on any profit you make, not on the total amount you receive. Moreover, HMRC has recently shed some light on DeFi (Decentralized Finance) activities, such as lending and staking. However, the details are still somewhat vague. The current guidance suggests that DeFi transactions could subject either to Income Tax or Capital Gains Tax, depending on what the transaction entails and if it’s considered a capital transaction or income-related activity.

Essentially, a capital transaction involves disposing of your crypto, even if you maintain the right to reclaim it. This might include:

- Contributing or withdrawing your crypto to a liquidity pool, especially if the DeFi protocol benefits from your liquidity.

- Staking your crypto via a DeFi protocol, though the rewards from staking could fall under Income Tax.

This emerging clarification from HMRC indicates that understanding the tax implications of your crypto, including “Bybit Tax in the UK”, especially with DeFi’s growing complexity, is crucial. The determination of the type of tax you owe depends on whether your transactions are seen as generating capital or income.

UK’s Crypto Capital Gains Tax rates

To file Bybit Taxes in the UK, you must understand the way Capital Gains Tax (CGT) works for your crypto gains is pretty straightforward because it doesn’t split rates into short-term and long-term like some other countries do. Your CGT rate hinges on your total income.

Here’s how it breaks down:

- 10% CGT Rate: Authorities tax your crypto gains at 10% if your income falls within the basic band, up to £50,270.

- 20% CGT Rate: For those in the higher (£50,271 to £150,000) or additional (over £150,000) income bands, the rate jumps to 20%.

So, based on your total earnings:

- Earn less than £50,270 in a year? Your crypto gains are taxed at 10%.

- Earn more than £50,270? Then you’re looking at a 20% tax rate on those gains.

Capital Gains Tax Rates for Crypto in the UK:

| Income Band | CGT Rate on Crypto Gains |

|---|---|

| Up to £50,270 | 10% |

| £50,271 to £150,000 | 20% |

| More than £150,000 | 20% |

Steps to Calculate crypto gains and losses

To file Bybit Taxes in the UK, Calculating your crypto gains and losses might sound complex, but it’s just about knowing a few key details. Here’s a simple breakdown to help you through it:

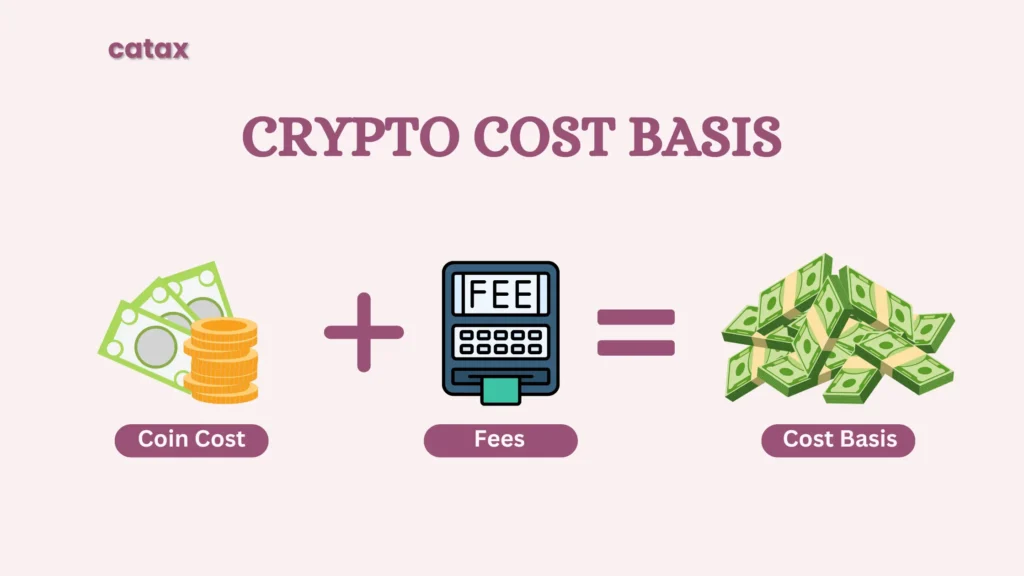

First, figure out your cost basis. This is just how much you originally paid for your crypto, including any fees. If your crypto came to you through an airdrop or fork, then use the value of the crypto in pounds on the day you got it.

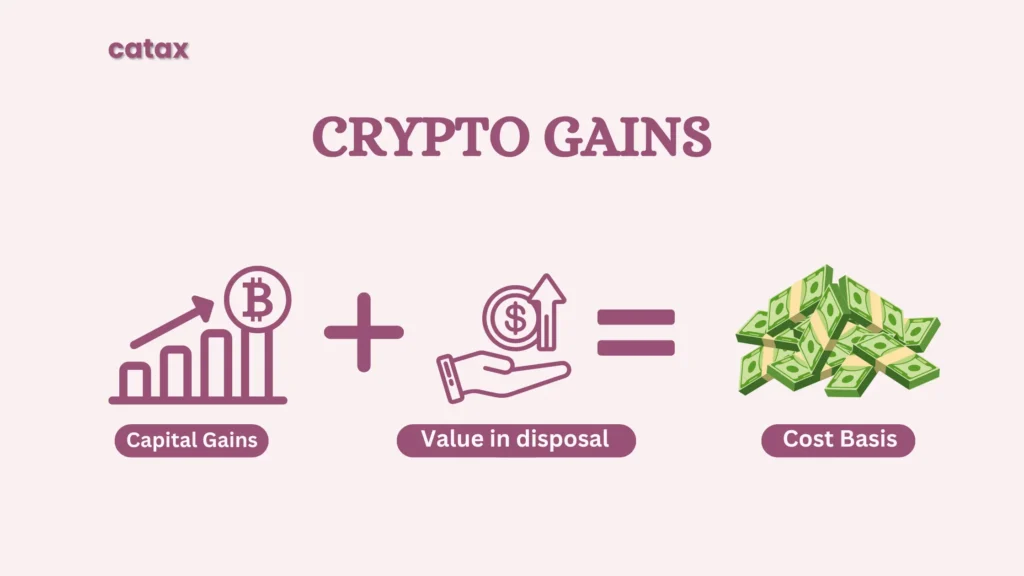

Once you’ve got your cost basis, you can easily work out if you’ve made a gain or a loss when you sell, swap, spend, or gift your crypto. Just subtract your cost basis from what you sold it for, or its value when you used it.

🔹 Capital Gains Tax applies if you make more money than you started.

🔹 If it’s less, you’ve made a loss, which might help reduce your tax bill later on.

Before we begin, remember the £12,300 capital gains allowance—you only pay tax on gains above this amount!

Example in a Nutshell

Imagine Oscar buys 1 BTC in May 2020 for £7,000 and pays an extra £100 in transaction fees. His total cost (cost basis) is £7,100.

Fast forward to May 2021, Oscar sells his BTC for £38,000. To find his gain, he subtracts his cost basis (£7,100) from his selling price (£38,000).

- Cost Basis: £7,000 (purchase price) + £100 (fees) = £7,100

- Sale Price: £38,000

- Capital Gain: £38,000 – £7,100 = £30,900

Before taxes, Oscar deducts his £12,300 allowance:

🔹 Taxable Gain: £30,900 – £12,300 = £18,600

Oscar’s income for the year is £70,000, putting him in the 20% Capital Gains Tax band. He’ll owe 20% of £18,600:

🔹 Tax Owed: £18,600 x 20% = £3,720

So, Oscar’s tax bill for his crypto gain is £3,720. This example shows how understanding your cost basis and using allowances can help figure out your crypto taxes.

Calculate CGT on cryptocurrency UK

To file Bybit Taxes in the UK, Figuring out your Capital Gains Tax (CGT) for cryptocurrency within the UK is not as daunting as it sounds. First up, you want to work out your fee foundation. This is just an elaborate manner of saying how a good deal you initially paid for your crypto, including any greater expenses. And if you acquire your crypto in a way that fails to contain shopping for it, like from an airdrop or fork, then you use the cost of the crypto in proper old British pounds at the day you obtained it.

Here’s a friendly step-through-step to see if you made a profit or a loss:

Finding Your Gain or Loss: This part deals with comparing the value of your crypto when you bought it to its value when you decided to sell, swap, spend, or gift it. Simply subtract your purchase cost (what you paid) from the crypto’s value when you let it go. If you end up with more money than you started, that’s a capital gain, and yes, you’ll need to give a portion of that to the taxman under “Bybit tax in the UK.” However, if you end up losing money, that’s a capital loss. Nobody enjoys losing money, but the upside is you don’t pay tax on losses, and they can even help lower your tax bill later on. street.

Let’s run via a short instance of crunching those numbers:

Tally Up Your Costs: Add up the whole lot you spent to acquire your crypto, now not forgetting any charges.

Do the Math on Your Profit or Loss: Subtract the price basis (your general spend) from the quantity you purchased when you offered or used your crypto.

Report What You Found: If you ended up making money, you’ll have to pay CGT on it. If you lose money, make sure to keep a record of it since it might lower your tax bill in the future.

Tax Breaks on Crypto

Alright, UK crypto buffs, particularly those trading on Bybit, here’s the lowdown on slashing your “Bybit tax in the UK” with some smart tax breaks.

£12,570 Income Tax-Free Sweet Spot: Your initial £12,570 of income in the UK, including from Bybit trades, stays clear of taxes. This gem helps you figure out your spot in the Income Tax bands by deducting this amount right off the top. Just a note, if your earnings exceed £125,140 annually, this tax break doesn’t apply.

Bag £1,000 (or Even £2,000) Tax-Free for Trading or Property: Dipping your toes in trading or property earnings? The first £1,000 you make is all yours, no tax, thanks to the Trading and Property Allowance. If you’re balancing both, you’re looking at a £2,000 tax-free bonus.

Capital Gains Tax-Free Allowance – A Biggie: Can’t stress this enough – the UK’s £12,300 Capital Gains Tax-Free Allowance is a boon. This means your capital gains from Bybit, up to £12,300 within a fiscal year, are yours to keep, no Capital Gains Tax required.

So, there you go – key tax breaks to help reduce your “Bybit tax in UK.” Make sure to leverage them and maximize your crypto earnings!

What Happened of tax on lost or stolen crypto in the UK

If your crypto goes missing or someone swipes it, HMRC has some guidelines that might feel like a bit of a puzzle.

Let’s talk about lost crypto first. Imagine you’ve lost the key to your crypto vault (aka your private key) and can’t access your digital treasure. You might think this loss could knock a bit off your tax bill, but it’s not that straightforward. Since the crypto is technically still out there in the digital ether, it’s not considered “disposed of” for tax purposes. But, don’t lose hope just yet! If you can convincingly argue that your digital gold is truly out of reach forever, you might be able to file what’s called a negligible value claim. If HMRC gives you the nod, you could then chalk up this digital disappearance as a capital loss.

Now, let’s talk about stolen crypto. You might think you can immediately count this as a loss, but HMRC sees it differently. Theft doesn’t automatically qualify you to claim a capital loss under “Bybit tax in the UK.” However, there’s a bit of hope in certain situations. For instance, if you paid for crypto on an exchange, but the crypto never arrived in your wallet due to a scam, you might qualify to make a negligible value claim. This could allow you to claim a capital loss later on.

So, while navigating the “Bybit tax in UK” waters can be tricky when your crypto vanishes or gets stolen, HMRC does offer a couple of lifelines to potentially salvage something for your tax situation.

Do I have to pay taxes when buying crypto?

To file Bybit Taxes in the UK, whether you owe taxes when buying crypto can depend on how you’re making the purchase. Let’s simplify this:

Buying Crypto with GBP: When you use good old British pounds (GBP) to buy your crypto, the taxman stays away. No taxes here! But, it’s super important to jot down every transaction. Keeping track of your buys helps you figure out your gains or losses when it’s time to sell.

HODling onto Your Crypto: Planning to hold onto your crypto and wait for its value to skyrocket? Good news – there’s no tax on just holding. Remember, though, to note down how much your crypto cost when you got it. This info is golden for later calculating any gains or losses.

Swapping Crypto for Crypto: If you’re swapping, say, your Bitcoin for Ether, the tax office wants a piece of any profit as Capital Gains Tax. HMRC sees swapping one crypto for another as a sale of your first crypto, which could mean tax time if you’ve made a gain.

Trading with Stablecoins: Stablecoins like USDT, which stick close to the value of fiat currencies like the US dollar, are a bit more stable. But trading crypto for stablecoins? That’s still a crypto-for-crypto swap in HMRC’s eyes, and profits might be taxable.

Do I have to pay taxes when buying crypto?

When it comes to transferring crypto, you’re in the clear tax-wise, as long as it’s between your wallets or exchanges. This is because HMRC doesn’t see this as selling your crypto, so no Capital Gains Tax applies here. It’s pretty much like shifting your pounds from one bank account to another.

Transferring Crypto in Wallet to Wallet: Moving your crypto stash around between your digital wallets? No problem. HMRC won’t ask for tax on these moves. But, remember, keeping tabs on these transfers is key, especially when it comes to any fees you might pay.

Paying Transfer Fees: Here’s where it gets a bit tricky. Your crypto platform might ask for a fee to move your crypto, and if you’re paying this fee in crypto, it counts as spending your crypto. This spending counts as selling crypto, which could result in tax time if you profit.

Example Time: Imagine you’ve snagged 2 ETH when the price was £2,500 per ETH, bringing your total spend to £5,000. You decide it’s time to shuffle this ETH from your Coinbase account over to Ledger for that extra security. Coinbase says, “Sure, but we’ll need 0.01 ETH for the transfer.”

Now, paying this fee with ETH means you’re parting with a slice of your digital pie. If the price of ETH hasn’t budged since you bought it, you’re looking at a fee value of £25 (0.01 ETH * £2,500).

Here’s the Crunch:

- You initially bought 2 ETH at £5,000.

- Your transfer fee is 0.01 ETH, valued at £25 at the time of the transfer.

You’re considering this £25 as a disposal of your crypto assets. While it might not immediately result in a capital gain or loss, HMRC must know. Keeping detailed records of these kinds of transactions ensures you’re all set for any checks or queries from them.

What About Adding or Removing Liquidity?

For those diving into the world of DeFi and liquidity pools, adding your crypto to these pools might not seem like a taxable event at first glance. However, HMRC views getting a liquidity pool token in return for your crypto as selling your crypto. So, you’ll need to calculate the cost of the crypto you put in and compare it to the value of the liquidity tokens you get. This will be important for when, or if, you decide to take your tokens out of the pool.

Keeping it Simple with Catax: Whether it’s transferring crypto, paying fees, or dealing with liquidity pools, keeping track of all these transactions can be a headache. But don’t worry, Catax has features like “treat transfer fees as disposals,” making it a breeze to stay on top of your “Bybit tax in the UK” obligations.

How are airdrops and forks taxed in the UK?

| Transaction Type | Tax Implications | Details |

|---|---|---|

| Soft and Hard Forks | Capital Gains Tax | No tax on receiving new coins from forks. However, when you sell, swap, spend, or gift these coins, they’re subject to CGT. |

| Receiving an Airdrop | Income Tax & Capital Gains Tax | Most airdrops are considered income and taxed accordingly. Later disposals of airdrop coins are subject to CGT. |

| Gifting Crypto to a Friend | Capital Gains Tax | Market value of crypto at the time of gifting is considered for CGT. If income tax has been paid on the gifted tokens, this value is adjusted in the CGT calculation. |

| Gifting Crypto to Spouse/Civil Partner | No Tax | Gifting to your spouse or civil partner is not taxable. However, they assume your cost basis when they dispose of the crypto. |

| Donating Crypto to Charity | No Tax | Donating crypto to a registered charity is not subject to tax. |

Navigating Crypto Mining and DeFi Taxes in the UK

To file Bybit Taxes in the UK, the way you’re taxed on crypto mining and your involvement in Decentralized Finance (DeFi) activities hinges on how HM Revenue & Customs (HMRC) categorizes your actions. Whether it’s a leisure pursuit or a business operation can significantly affect your tax obligations.

Mining Cryptocurrency as a Hobby vs. a Business

Your mining activity might be a mere hobby or a serious business venture, depending on:

- How much effort you put in

- The level of organization

- The risks involved

- Whether it aims to make a profit

For Hobby Miners: If you mine crypto as a hobby, you’ll need to report any earnings under “miscellaneous income” on your tax return. Your income is essentially the market value of the crypto at the time you receive it, converted to GBP. While you can deduct certain costs before adding this income to your total taxable income, remember, that any profit from selling this crypto later will attract Capital Gains Tax.

For Business Miners: When mining is considered a business, all income from mining, including fees or rewards from mining or staking activities, is added to your trading profits, subject to Income Tax. You’re also allowed to deduct relevant expenses. Upon disposing of the mined cryptocurrency. Any increase in value from the time of acquisition to sale is considered part of trading profits. Attracting both Income Tax and National Insurance contributions.

DeFi and Taxation in the UK

DeFi, while a relatively recent phenomenon, has caught the attention of HMRC. Their guidance, as of February 2022, attempts to clarify tax obligations but ends up leaving much to individual interpretation, focusing on the “nature of the transaction” to determine if it falls under Capital Gains Tax or Income Tax.

DeFi Transactions Considered Disposals: Your DeFi transactions, like adding or removing liquidity and staking crypto, might now be seen as disposals, subject to Capital Gains Tax. This also applies to rewards from DeFi protocols, especially if received as a lump sum.

Returns from DeFi as Income: However, returns from DeFi might be classified as income, particularly if:

- The return amount is predetermined.

- It’s paid by the borrower or DeFi platform.

- It’s distributed periodically during the lending/staking period.

Earnings from new tokens or coins are acquired periodically through. DeFi activities are likely viewed as income and are taxable under Income Tax for Bybit tax in the UK.

Key Takeaways:

- Determine whether your crypto mining is a hobby or business to understand your tax duties.

- For hobby mining, report earnings as “miscellaneous income.”

- Business mining income is added to trading profits, subject to Income Tax.

- In DeFi, the nature of transactions dictates whether they’re taxed as capital gains or income.

Navigating the complexities of crypto mining and DeFi taxes in the UK requires a detailed understanding of HMRC’s guidelines. Keeping accurate records and understanding the nature of your transactions will help ensure compliance and potentially minimize your tax liabilities.

File Your crypto taxes with paper forms

- Calculate Your Crypto Taxes: You’ll need to know your capital gains, losses, and any income or expenses related to your crypto activities. Catax streamlines this step by crunching those numbers based on your transaction history.

- Register for Online Filing Early: If you’re new to this, make sure to register for the Government Gateway service by October 5, 2024. This registration is key to accessing the forms you’ll need to file online.

- Tackle the SA100 Form: This Self Assessment Tax Return form is where you’ll report any income from your crypto activities, right in box 17. Catax’s detailed reports can help you fill this out accurately.

- Don’t Forget About Capital Gains: If you’ve realized any capital gains from your crypto investments, tick “yes” in box 7. This action also requires you to fill out the supplementary Self Assessment: Capital Gains Summary (SA108) form.

- Submit Before the January Deadline: Ensure your Self Assessment Tax Return is submitted online to HMRC by midnight on January 31, 2025.

What kind of records might HMRC ask for?

As far as crypto record keeping is concerned, HMRC correctly states that many exchanges do not keep detailed information about crypto transactions and the onus of maintaining these transactions accurately rests with the taxpayer. These details include:

- the type of crypto asset

- date of the transaction

- whether the crypto assets were bought or sold

- the number of units involved

- value of the transaction in pound sterling

- The cumulative total of the investment units held

- bank statements and wallet addresses, as these might be needed for an enquiry or review

Cost Basis Method of UK

They refer to this as the share pooling method, designed to ensure a fair assessment of your crypto gains and losses, especially concerning Bybit Taxes in the UK. Let’s delve into the three key rules you’ll need to follow:

Same-Day Rule: Were you actively trading the same cryptocurrency on the same day? Here, you calculate gains or losses using the cost basis of transactions made on that particular day. If your sales exceed your purchases, then you’ll proceed to the next rule for the excess.

Bed and Breakfasting Rule: This rule applies to those who sell and then buy back the same crypto within a 30-day window. For such transactions, you use the cost basis of the repurchased crypto to determine your gains or losses. If you’re still selling more than you’re buying in this timeframe, it’s time to move to the last rule.

Section 104 Rule: When the first two rules don’t apply to some of your transactions, this is your go-to method. It’s somewhat similar to the ACB (Adjusted Cost Base) method. You’ll calculate an average cost basis for all your crypto assets in a ‘pool’. Just add up what you’ve paid for all assets and divide by the total number of coins or tokens you have.

Understanding these rules helps ensure you’re accurately reporting your crypto taxes, particularly those related to Bybit, in the UK, and avoiding any potential pitfalls with HMRC.

Navigating the maze of cryptocurrency taxes in the UK can feel like a daunting task, but there are legit ways to potentially lower your tax bill without stepping over any legal lines. If you’re aiming for a more tax-efficient 2023, here’s what you could consider doing before the financial year wraps up on April 5, 2022.

How Can I avoid my Crypto taxes in the UK?

- Wait It Out: Holding onto your crypto for at least a year can sometimes offer tax benefits, thanks to long-term capital gains rules.

- Use Tax-Free Allowances: The UK offers a Capital Gains Tax allowance, meaning you only start paying tax on gains above a certain threshold. Make sure you’re utilizing this to its fullest.

- Pension Pot Investments: You can invest your crypto gains into a pension fund, potentially deferring or reducing the tax due while saving for retirement.

- Adjust Your Tax Rate: If possible, adjust your tax rate by managing how much taxable income you take each year. This could mean selling assets in a year you’re earning less.

- Charitable Contributions: Donating crypto to charity can reduce your taxable income. You may not be taxed on the donated amount and might even qualify for additional tax relief.

- Gifts to Others: Gifting crypto to your spouse or civil partner can transfer the asset without immediate tax implications, though the recipient might face taxes upon eventual sale.

- Look into Opportunity Zone Funds: While more applicable in the U.S., the UK might have similar schemes that offer tax advantages for investments in certain areas or industries.

- Spotting Losses with a Crypto Calculator: Use a crypto tax calculator to identify any losses that can offset your gains and lower your tax liability.

- Write Off Dead Coins: If you hold cryptocurrency that has become worthless or inaccessible, you may be able to claim a loss, reducing your overall taxable gains.

- Choose Your Moment: Selling your crypto in a year when your overall income is lower can mean paying a lower tax rate on your gains.

Navigating Your Bybit Taxes in the UK with Catax: Simple Steps

Navigating your Bybit Taxes in the UK with crypto tax software like Catax can be accomplished with just a few steps.

- Link Catax and Bybit Accounts: To seamlessly integrate your transactions, effortlessly connect your accounts with both Bybit and Catax. By simply generating API keys, your data will be shared with utmost security and precision.

- Import Your Transactions: Connecting to Catax will instantly retrieve your complete transaction history from Bybit. This includes all trades, deposits, and withdrawals. It’s important to give the imported data a thorough review for accuracy.

- Examine Your Transactions: Examine the comprehensive data collected by Catax carefully. Awareness of any inconsistencies is crucial to guarantee the precision of your tax filing.

- Select Your Tax Year: The tax year in the UK begins on April 6th and ends on April 5th of the following year. Selecting the appropriate tax year for your report to meet the expectations of HM Revenue and Customs (HMRC) is important.

- Generate Your Tax Report: Allow Catax to effortlessly compute and consolidate a detailed tax report just for you. This comprehensive report will meticulously outline your capital gains and losses, earnings from cryptocurrency transactions, and potential deductions. Walk away with peace of mind and let Catax handle the rest.

- Review Your Report Thoroughly: Before submitting your Catax-generated report, it is imperative to review it for any discrepancies thoroughly. Ensuring that all information is accurate will prevent any complications with HMRC.

- Submit to HMRC: Once you have finalized and confirmed your report, go ahead and submit it to HMRC. This may be incorporated into your Self-assessment tax return. Depending on your circumstances. It’s crucial to adhere to the deadline of January 31st for online submissions to avoid facing penalties.

Why This Matters in the UK:

Keeping up with your Bybit tax in the UK ensures compliance with HMRC regulations, avoiding potential fines or audits. Catax simplifies this process, making tax reporting more manageable and helping you navigate the complexities of cryptocurrency taxation.

Frequently Asked Question(FAQs)

The tax rate for cryptocurrency transactions in the UK varies based on your total income. Tax authorities can levy capital gains tax rates ranging from 10% to 20%, while they can impose tax rates ranging from 20% to 45% on additional income from cryptocurrency.

Stay informed about evolving cryptocurrency tax laws, identify deductible expenses associated with crypto transactions, be aware of the capital gains allowance, maintain detailed records for at least five years, and consider using HMRC’s real-time CGT reporting service.

Catax can streamline calculating and reporting crypto taxes by integrating with Bybit accounts, importing transaction data, generating detailed tax reports, and providing expert guidance on compliance with HMRC regulations.

Crypto investors in the UK can report their gains on their annual self-assessment tax return or use HMRC’s real-time CGT reporting service. Keeping accurate records of transactions, including types of tokens, dates, quantities, values, and associated bank statements, is essential for tax compliance.

HMRC treats cryptocurrency as a capital asset, subjecting gains to Capital Gains Tax (CGT). The CGT rate depends on your income level, with rates of 10% or 20% for gains.